Lending has by far been the most important use case for onchain finance. Onchain lending brings a new dimension to how we think about liquidity, collateral, and risk management for credit, and these functions are governed by the market structures we design.

In lending protocols, market structure defines how borrowing, lending, liquidity, collateral, and risk are organized. Common structures include pool-based or peer-to-peer markets, isolated or shared collateral markets, and fixed or variable interest rate systems.

Aave itself evolved from fixed-rate peer-to-peer lending markets (then known as ETHLend) into pooled markets, and is now expanding into an all-in-one modular architecture with Aave V4.

Liquidity coordination costs

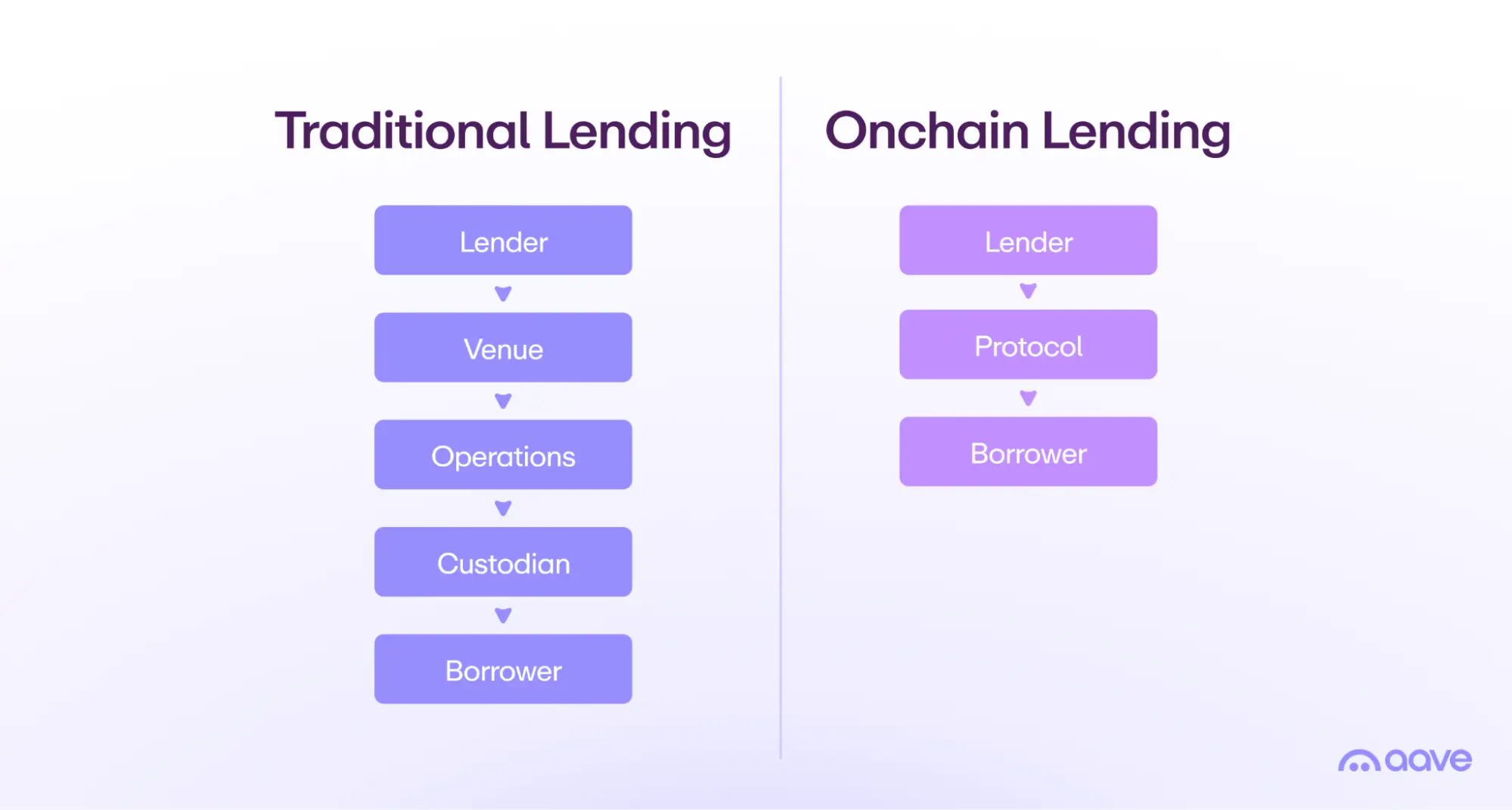

At its core, onchain lending improves liquidity coordination costs that often arise from inefficiencies. For example, in traditional lending, they come from the segregation of venues, capital, and users, or from settlement frictions such as back-office costs.

Onchain lending compresses these coordination costs by moving much of the traditional lending stack from manual, repetitive work into codified smart contracts, improving automation and capital aggregation. This is achieved through the open networks, transparency, and execution guarantees that DeFi provides.

How market structures affect liquidity coordination costs

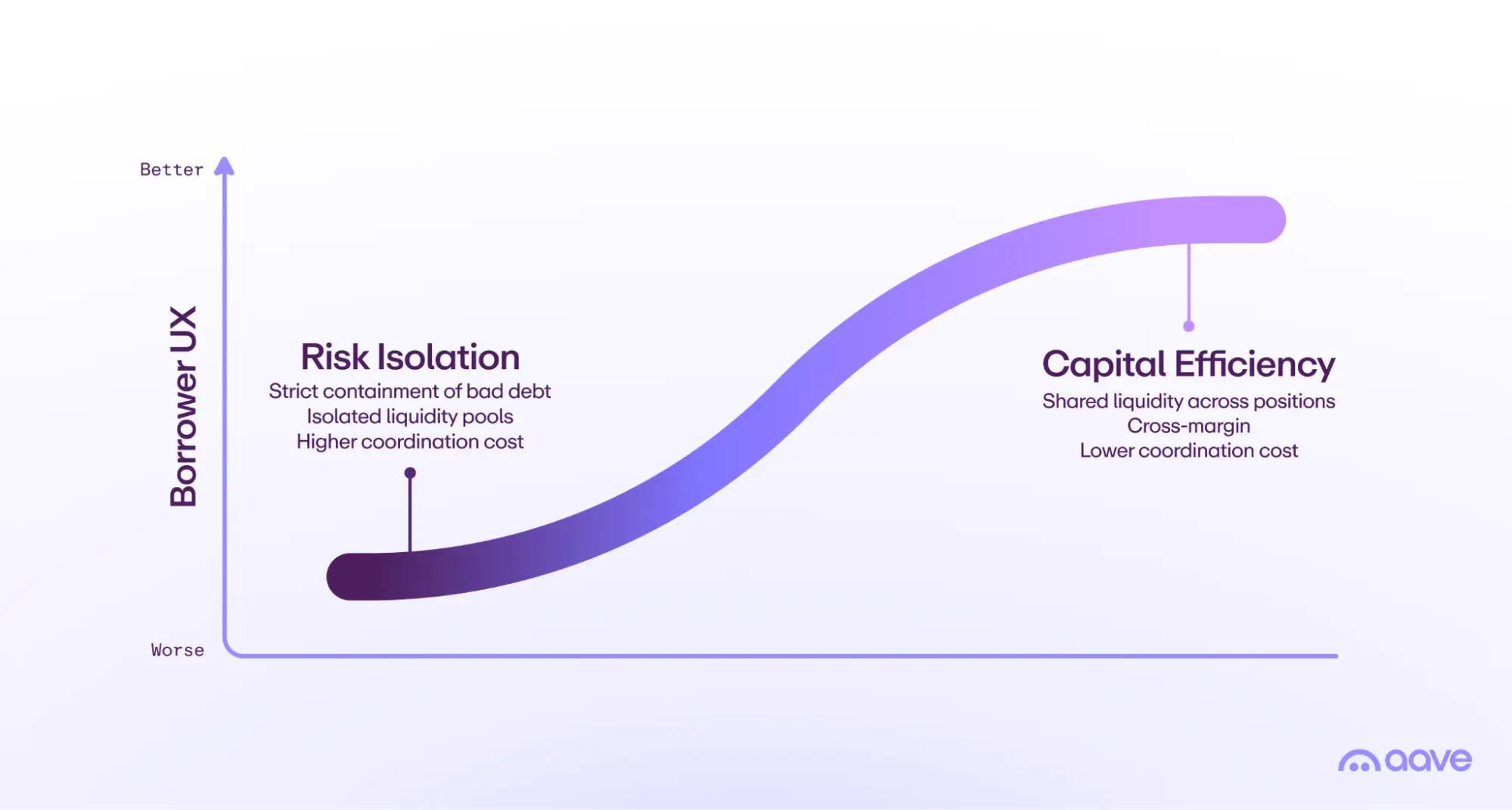

Good market structure design ensures liquidity efficiency and reduces fragmentation and pricing dislocations, bringing better pricing and lower liquidity risk for users. At the same time, good lending market structure design ensures sufficient risk management, including risk isolation and collateral redeemability.

There is no one-size-fits-all model in lending; the right structure depends heavily on use cases and objectives. Typically, the optimal point for any market structure is to organize liquidity as efficiently as possible to minimize coordination costs without introducing excess risk into the system.

Risk isolation and capital efficiency exist on a spectrum. Moving toward isolation reduces capital efficiency and weakens liquidity network effects, adding coordination costs. Borrower experience, conversely, improves with capital efficiency and degrades with isolation.

We believe the future of onchain lending requires a flexible, modular architecture that supports market structures placing users and use cases across the risk spectrum, depending on their return expectations.

What market structure designs does Aave V4 enable?

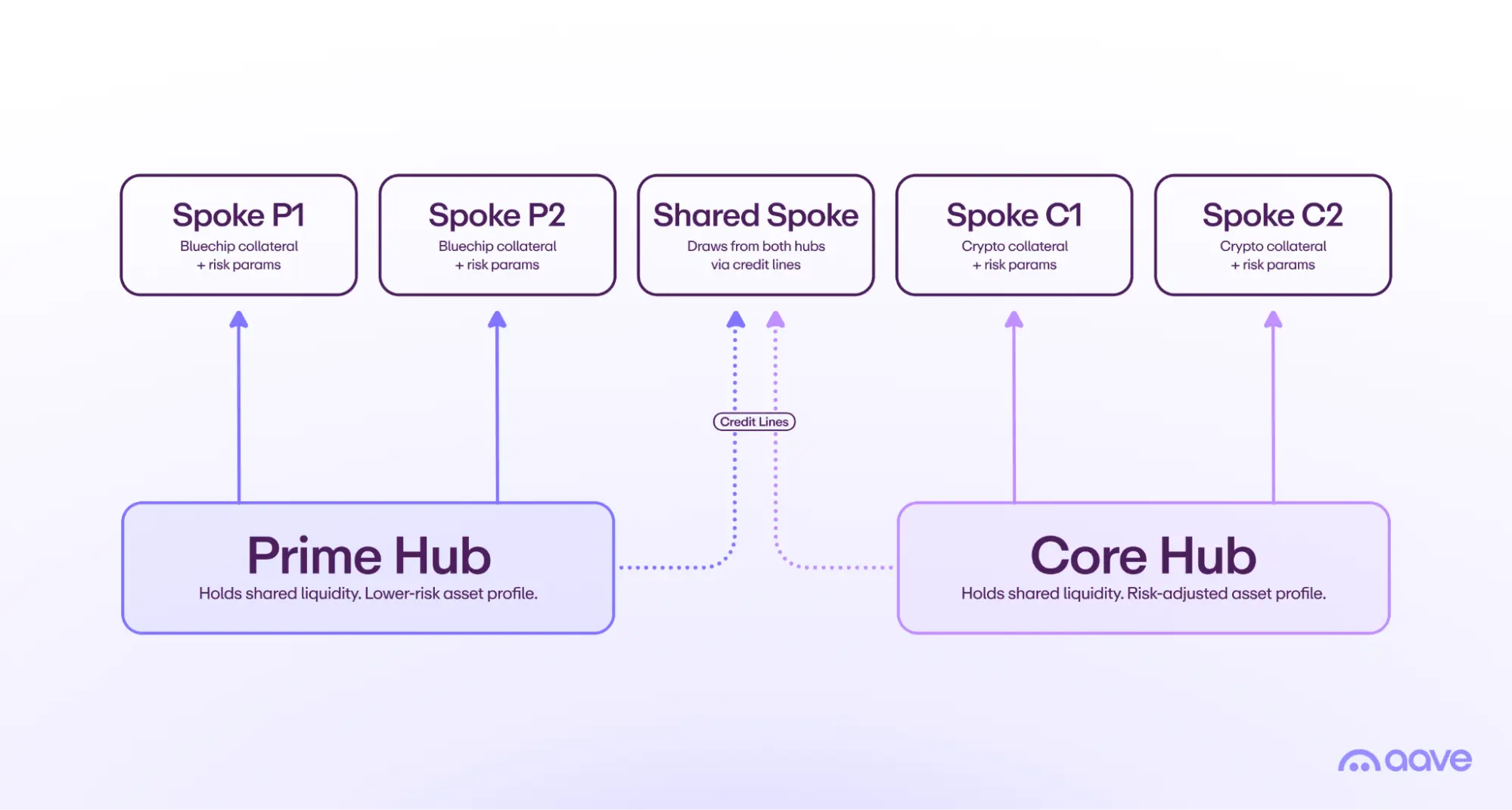

Aave V4 is designed around a Hub and Spoke architecture. A Hub and its Spokes together form a "market" or "venue." A Spoke is itself a borrowing market, while a Hub is where liquidity is stored and made available to Spoke borrowing markets through credit lines. Spokes manage all asset listings and their borrowing parameters, such as the Collateral Factor (CF), which defines how much a borrower can borrow against their collateral. Notably, a single Hub and Spoke pairing is not the whole market structure, since you can also run multiple segregated Hubs, such as Prime, Core, and Plus, to establish a risk curve.

Market structure design itself sets the bounds for organizing risk and liquidity onchain. Aave's motivation for iterating toward the new Hub and Spoke direction is the flexibility it provides for market structure design.

We believe onchain lending will support many different approaches, just as lending does in the current financial system. Serving those use cases takes infrastructure built for them, whether they're DeFi-native, real-world assets (RWAs), or credit more broadly.

Aave V4 market structures

Paired asset market

A paired asset market is the most basic market structure for onchain lending, where one collateral asset backs the borrowing of a single other asset. The arrangement works much like centralized overcollateralized crypto lending.

The benefit of this market structure is its simplicity. With no cross-margin, it can be easier for borrowers to unwind their collateral, since collateral is directly available. The downside is that, without cross-margin, lenders have no excess liquidity coming from other cross-collateralized use cases. This increases liquidity risk and makes it harder for lenders to unwind their positions. Bootstrapping initial liquidity, or supplying additional liquidity as demand increases, also carries higher coordination costs.

A paired asset market fits well for use cases at the tail end of the risk curve, where risk segregation is paramount, though it comes with the highest liquidity coordination costs.

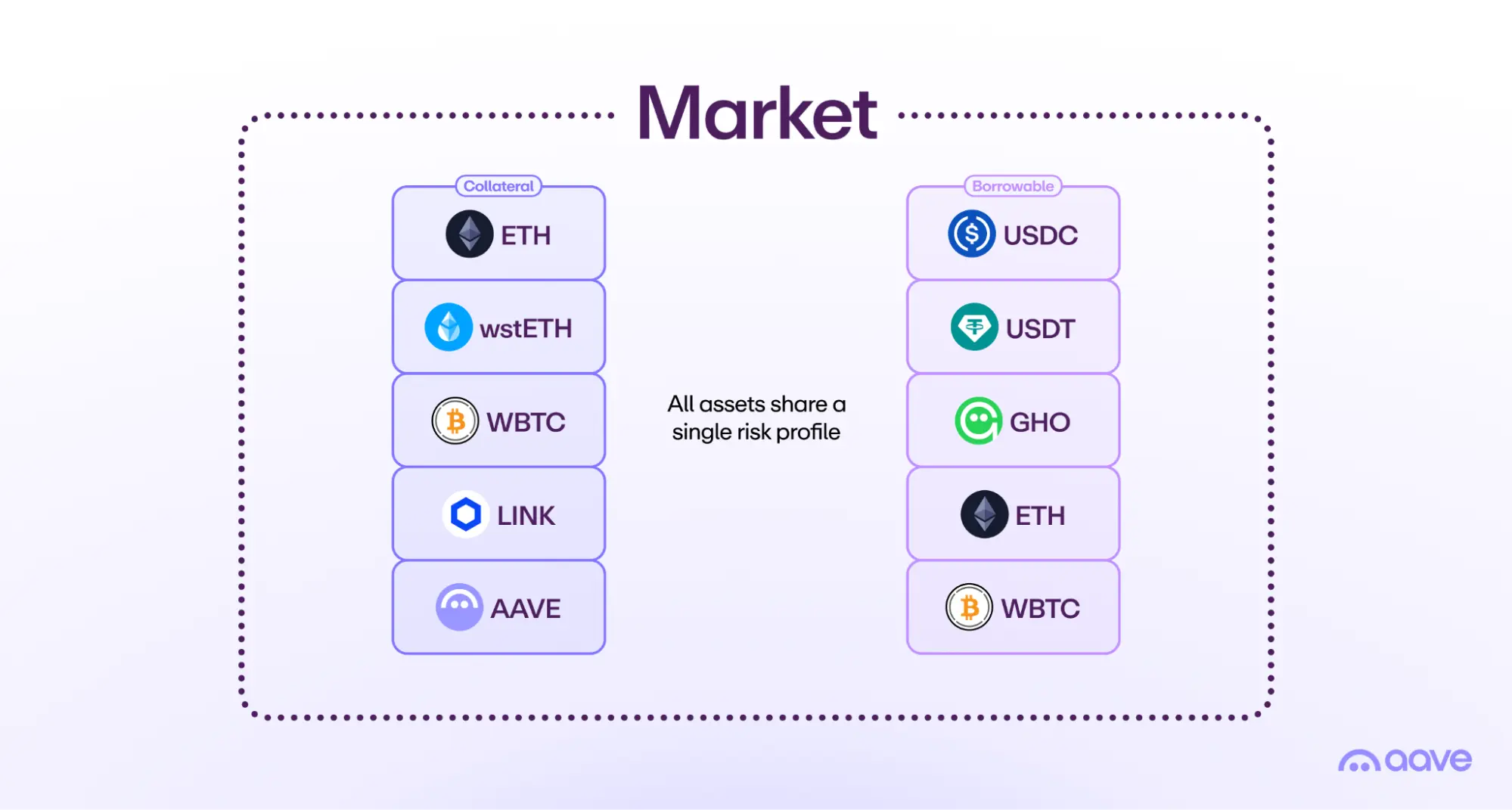

Multi-asset collateral singleton market

In a multi-asset collateral singleton market structure, a single market supports multiple collateral assets and one or many borrowable assets. The most successful example of this is the Aave V3 market structure, which is by far the most effective design we've seen for reducing liquidity coordination costs.

Within this market structure, collateral assets may or may not be borrowable, depending on market preference, use cases, and capital efficiency considerations. The result can be highly capital efficient, providing good pricing and liquidity for users.

The downside is that it aggregates everything into a single risk profile. In Aave V3, this can be refined through eMode, which creates pockets within the market with more granular risk parameters. For example, adjusting how much can be borrowed against a given collateral asset for specific use cases like borrowing against correlated assets.

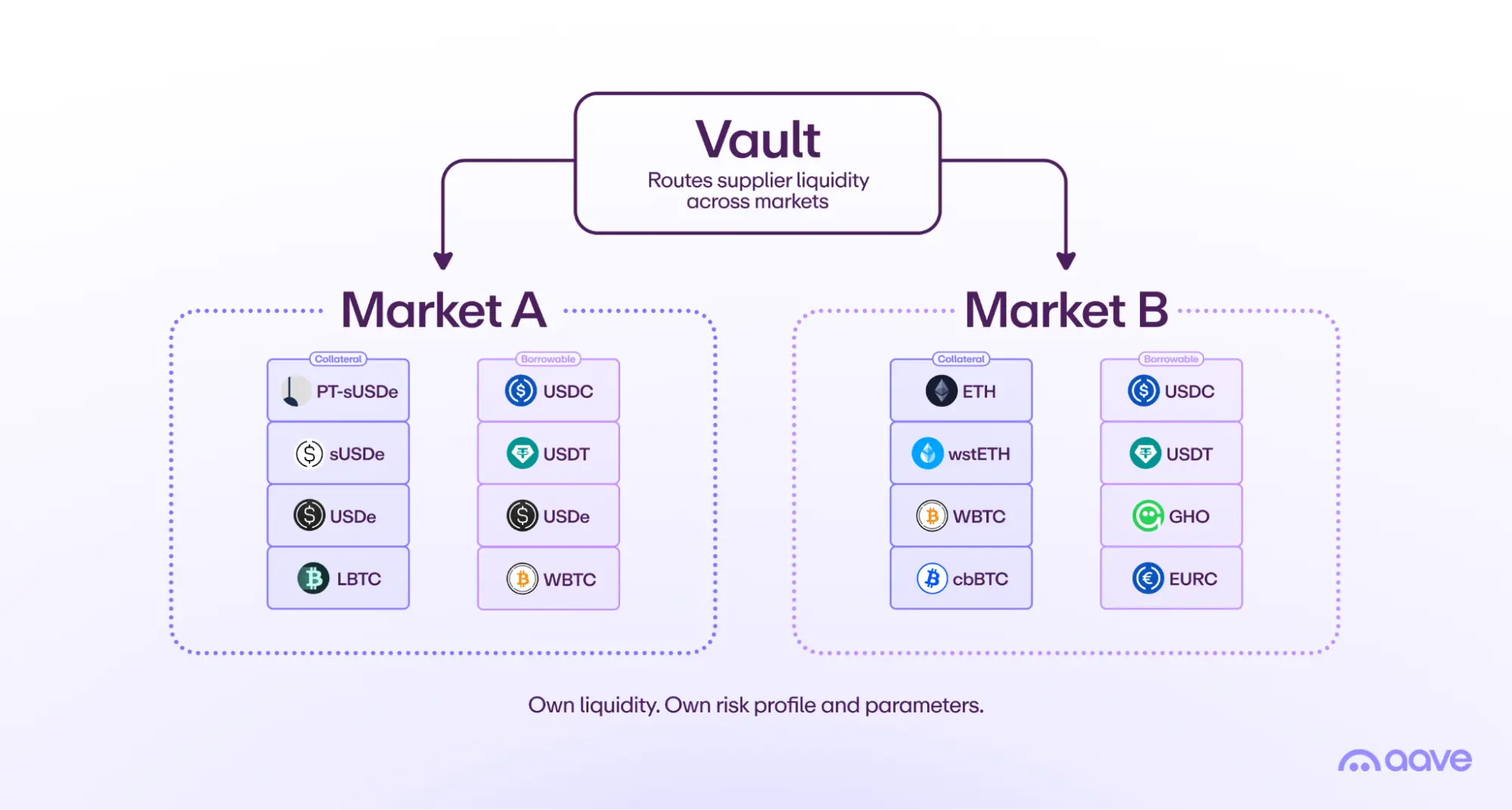

Multi-asset segregated market

The singleton model can be adjusted from a risk standpoint by deploying multiple singleton markets, each with its own risk profile derived from its collateral assets, borrowable assets, and parameters.

This approach creates a risk curve and gives lenders a choice: supply to a low-risk market or to a risk-adjusted one. Risk is isolated within each market.

The downside is that liquidity becomes siloed between markets, creating coordination costs and capital inefficiencies. This model is well suited for use cases whose risk profiles differ substantially from one another.

Vaults can be used either to enhance the risk profile, by supplying to both markets to diversify exposure, or to improve liquidity coordination for the lender, less so for the borrower. Fragmentation still persists for borrowers: if a borrower holds two collateral assets and needs to borrow from two separate markets, they must monitor multiple positions.

Multiple separate markets can be easily structured on Aave by deploying several singleton markets (as in Aave V3), or by running multiple vanilla Aave V4 Hub and Spoke configurations without credit lines between them.

Multi-asset segregated markets with credit lines

In this market structure, each market is segregated. In Aave V4, that separation is achieved through Spokes, which define the collateral set and risk parameters for each market, while the Hub holds the underlying assets. Spokes can be connected to Hubs that allow asset-by-asset credit lines to be drawn by the Spoke up to a maximum cap, enabling access to liquidity.

This makes it possible to cap each asset's exposure per market, establishing a total exposure ceiling per Hub for each asset. In a scenario where an asset in a Spoke becomes unbacked, contagion is bounded by the maximum exposure set by the credit lines.

Credit lines enable market structures that segregate markets while still reducing liquidity coordination costs for users. One example use case for credit lines is seeding liquidity from a risk-adjusted market like Core into a lower-risk market like Prime, improving coordination costs along the risk curve.

Another example: instead of listing an asset in the Core market via eMode as in Aave V3, a new Hub can be placed higher on the risk curve, with a Spoke listing the asset and drawing a credit line from Core to seed its liquidity. Compared to previous iterations of Aave, this means any lent asset can be fully capped at a maximum exposure.

This "hybrid" model allows for running an onchain loan book with capital efficiency, while segregating risk between markets and limiting Hub exposure through credit lines. If a Spoke's asset becomes unbacked, a Hub can simply disable the credit line; beyond that line, exposure is bounded.

RWAs particularly benefit from this model, since onboarding them requires both capital bootstrapping and a carefully designed market structure for risk controls. For example, a Hub could include Spokes for specific asset classes such as equities, private credit, and alternative funds, each with carefully tailored risk parameters and limited credit lines from the Hub.

Existing deep-liquidity Aave markets, backed by crypto collateral and stablecoin reserves, can be used to bootstrap RWA and credit use cases with lower liquidity coordination costs than traditional finance.

While good market structure can organize liquidity and risk, full due diligence on asset listings remains essential to ensure proper parameterization of the loan book. These examples show how market structures can be designed and supported within Aave V4, while not exhaustive, it covers a wide range of use-cases including institutional.