Securities finance is one of the largest markets that almost nobody outside Wall Street thinks about, and it is already starting to move onchain. Lending against securities collateral is a multi-trillion-dollar business. Repo alone averages around $12.6 trillion in daily exposures in the U.S., margin lending sits at a record $1.3 trillion, and wealth-management securities-based loans add over $400 billion on top of that. Securities lending, counted separately, keeps roughly $4.6 trillion of assets on loan and generated a record $15 billion in revenue in 2025. Almost none of this activity touches a blockchain today, which presents an opportunity.

The best way to move it onchain is to get the market structure right. Between the borrower and the lender sits a stack of custodians, lending agents, tri-party collateral managers, prime brokers, and clearing houses. Each layer of the stack takes a fee, adds a settlement delay, and obscures information. Collateral gets trapped inside bilateral relationships, rehypothecation chains stretch out of view, and when something fails, nobody can see why for days. Every level of the stack creates work, friction, and cost.

Improving that market structure is what Aave V4 is built to do, and the onchain rails are already at scale. The stablecoin market has crossed $322 billion, Aave secures roughly $23 billion in liquidity, GHO is live as a native dollar for Aave, and Aave Horizon is past half a billion dollars in total deposits powering RWA-backed loans. The cash leg, the liquidity, and the collateral pipeline all exist now.

Why V4 fits

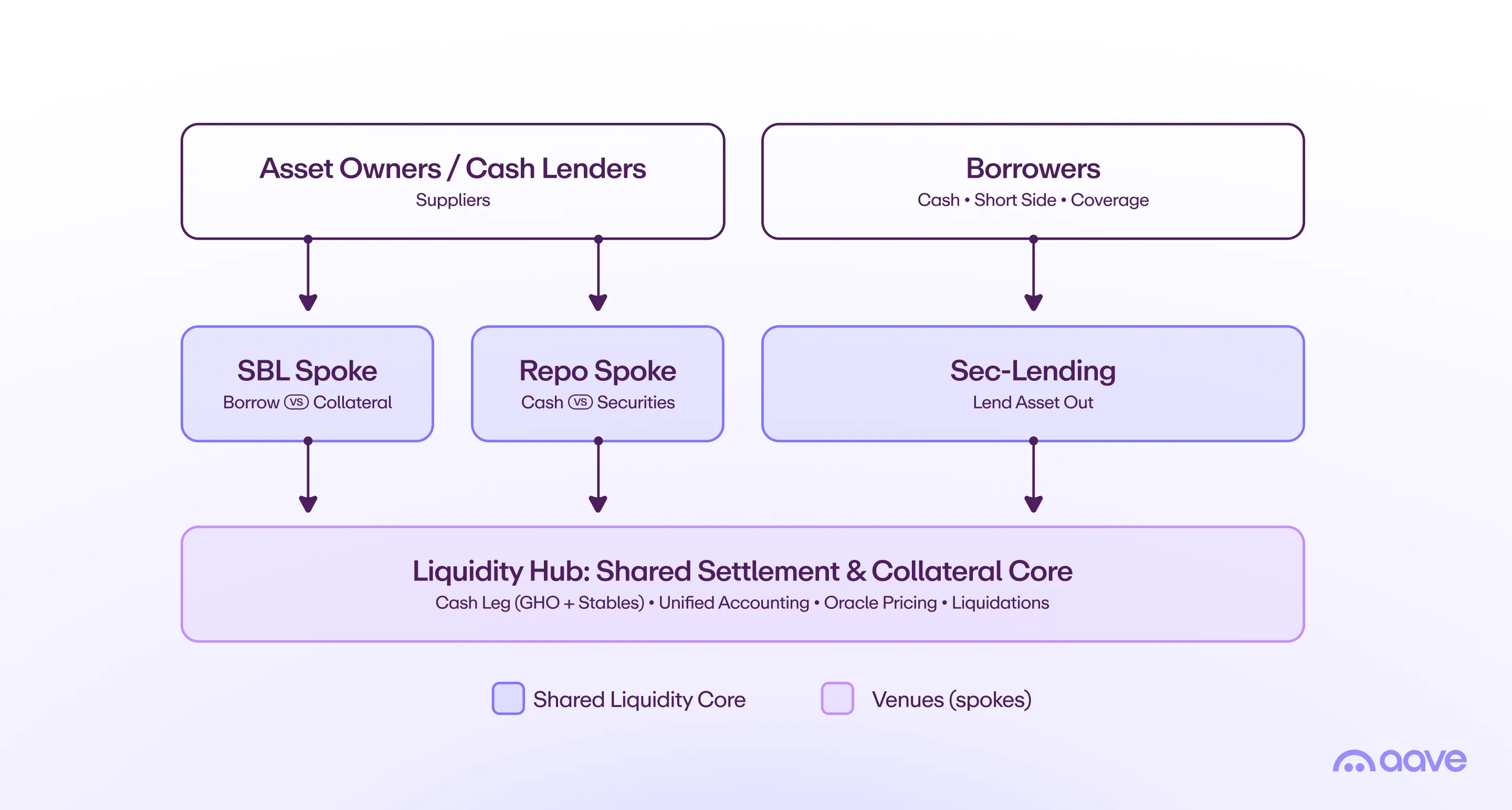

V4 separates the system into liquidity hubs and spokes. A hub is a deep pool of capital, and spokes are the modular venues (i.e. markets) that plug into it, each with its own risk parameters, asset scope, and rules. That single design choice maps almost perfectly onto how a securities financing market wants to be organized, with shared liquidity underneath and segmented, compliant venues on top.

Three flows run through it, and together they are the market.

Securities backed lending

A tokenized security is posted as collateral in a spoke with conservative, asset-specific haircuts, and the owner borrows GHO or stablecoins against it without selling. The position stays transparent, the haircut is explicit, and liquidation runs automatically rather than through a back office. The owner keeps the upside and unlocks the liquidity, and the bank balance sheet is freed up. This is already a $400 billion book in U.S. wealth management alone and still undeserved, and as real-world assets tokenize toward $16 trillion by 2030, every one of those assets becomes collateral that can be borrowed against instantly. Horizon has already grown past half a billion dollars in institutional RWA deposits, so the demand is clear. For the end user, liquidity arrives in minutes against tokenized collateral instead of through a bilateral facility negotiated over days, and the rate is transparent and set by a deep shared pool.

Repo

This is the giant. Repo is short-dated, collateralized cash borrowing, mostly against Treasuries, and the U.S. market alone averages around $12.6 trillion in daily exposures. Onchain, repo is simply borrowing the stablecoin cash leg against tokenized securities in a low-risk hub, which is exactly what V4 is built to do. Atomic delivery-versus-payment removes settlement fails, terms become programmable and can run 24/7 rather than on the banking calendar, and the roughly $5 trillion of opaque non-centrally-cleared bilateral repo becomes transparent and continuously margined. The market that most needs clean settlement and live collateral visibility is the one V4 serves best.

Securities lending

The tokenized security itself becomes a borrowable asset in a hub. Borrow demand from the short side and the settlement-coverage side pays a rate that flows straight back to the suppliers who own the asset, and the lending-agent function of matching, pricing, and collateral management collapses into the protocol. This is where the fee pool sits, with $15 billion in 2025 revenue against tens of trillions in lendable supply. Today lending agents keep roughly 20 to 30 percent of that revenue, several billion dollars a year skimmed before the owner sees a cent. Route the same flow through a protocol and that take compresses toward zero, with the spread accruing to the owner instead.

A proposed market structure

There are two ways to lay this out, and both share the same spokes. They differ only in how the liquidity underneath is organized.

Option A: one shared Liquidity Hub

A single liquidity hub acts as the settlement and collateral core. It holds the cash leg, keeps unified accounting of every position, prices collateral through oracles, so maximum depth lives in one place and is shared by everything above it.

Around it sit purpose-built spokes, each a venue with its own rulebook but the same liquidity underneath. An SBL spoke accepts tokenized securities as collateral and lets owners draw stablecoins or GHO against conservative, asset-class haircuts. SBL spoke can be divided into multiple spokes, depending on the risk. A repo spoke handles short-dated collateralized cash borrowing against high-quality securities, atomically settled and continuously margined. A securities-lending spoke lists tokenized securities as borrowable assets, with the borrow fee routing to the owners who supply them.

The strength of this layout is depth, since one pool means the deepest possible liquidity and the simplest accounting. The limitation is that risk lives in one place, so isolation has to be engineered at the spoke layer rather than being structural.

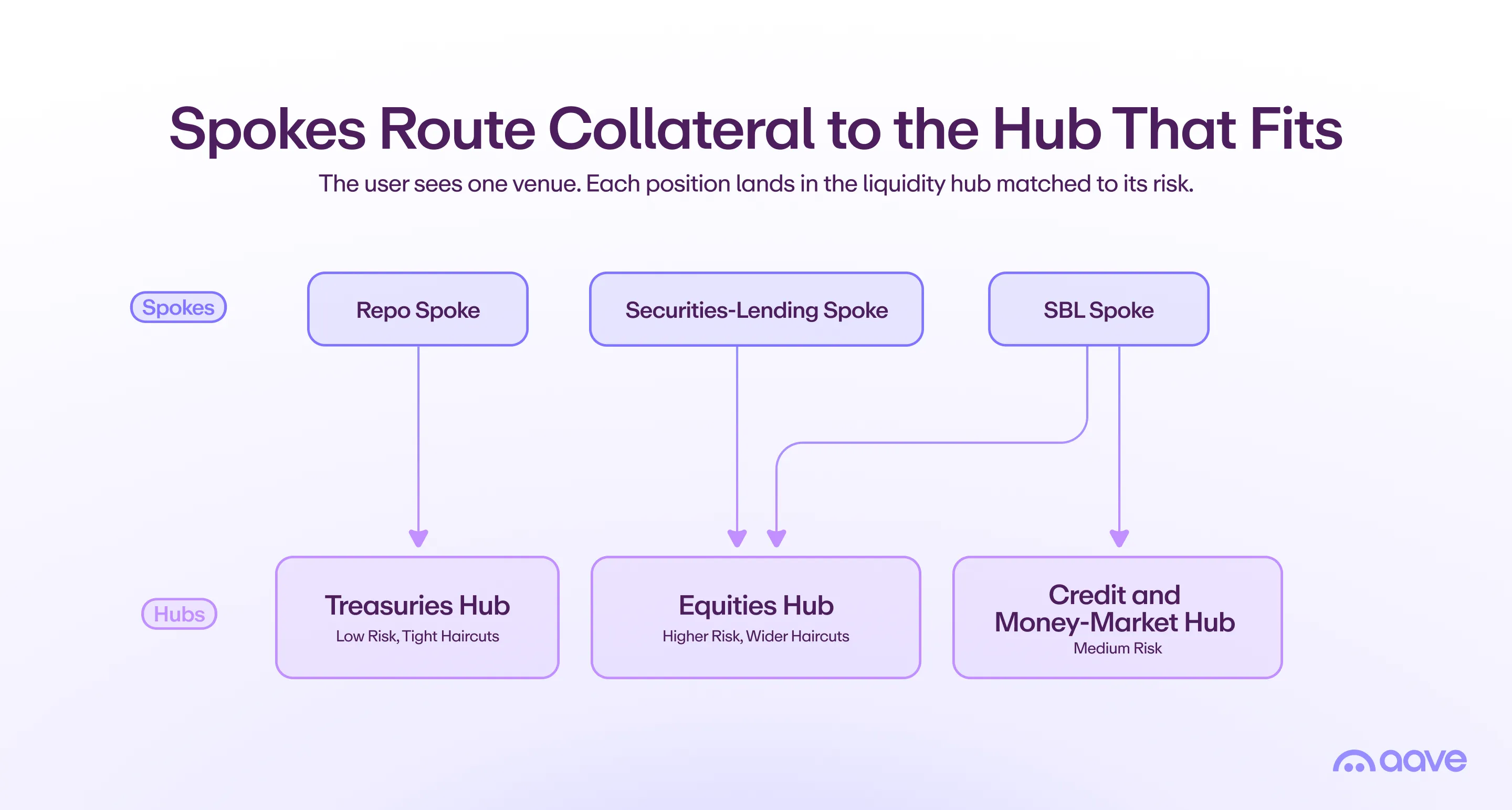

Option B: multiple hubs by asset category and risk

The alternative is to run several liquidity hubs, each scoped to an asset category and a risk profile, and let spokes connect to more than one at once. A low-risk treasuries hub with tight haircuts is where most repo naturally lands, a medium-risk credit and money-market hub serves other needs, and a higher-risk equities hub carries wider haircuts and stricter liquidation thresholds. Each hub prices and isolates its own risk.

The spokes route across these hubs automatically. The repo spoke sends Treasury collateral to the treasuries hub, the SBL spoke sends an equity basket to the equities hub, and the same user sees one venue while the protocol places each position in the pool whose parameters fit.

This buys three things. Risk isolation becomes structural rather than configured, so a shock in equities can be contained without ever touching the treasuries pool that backs repo. Pricing gets sharper, because each hub sets rates and haircuts for one risk profile instead of blending many. And regulatory separation gets easier, since a hub can be scoped to a single regime while spokes still aggregate the experience across all of them. The tradeoff is shallower depth per hub, but because spokes pull across multiple hubs, aggregate liquidity and composability are preserved. Credit lines between hubs to particular Spokes can increase the liquidity flow while preserving risk isolation exposure up to the credit line.

The practical path is a spectrum rather than a binary. Start unified for depth and simplicity, then graduate to category-and-risk hubs as collateral types scale and isolation becomes worth the fragmentation. The same spokes carry over either way.

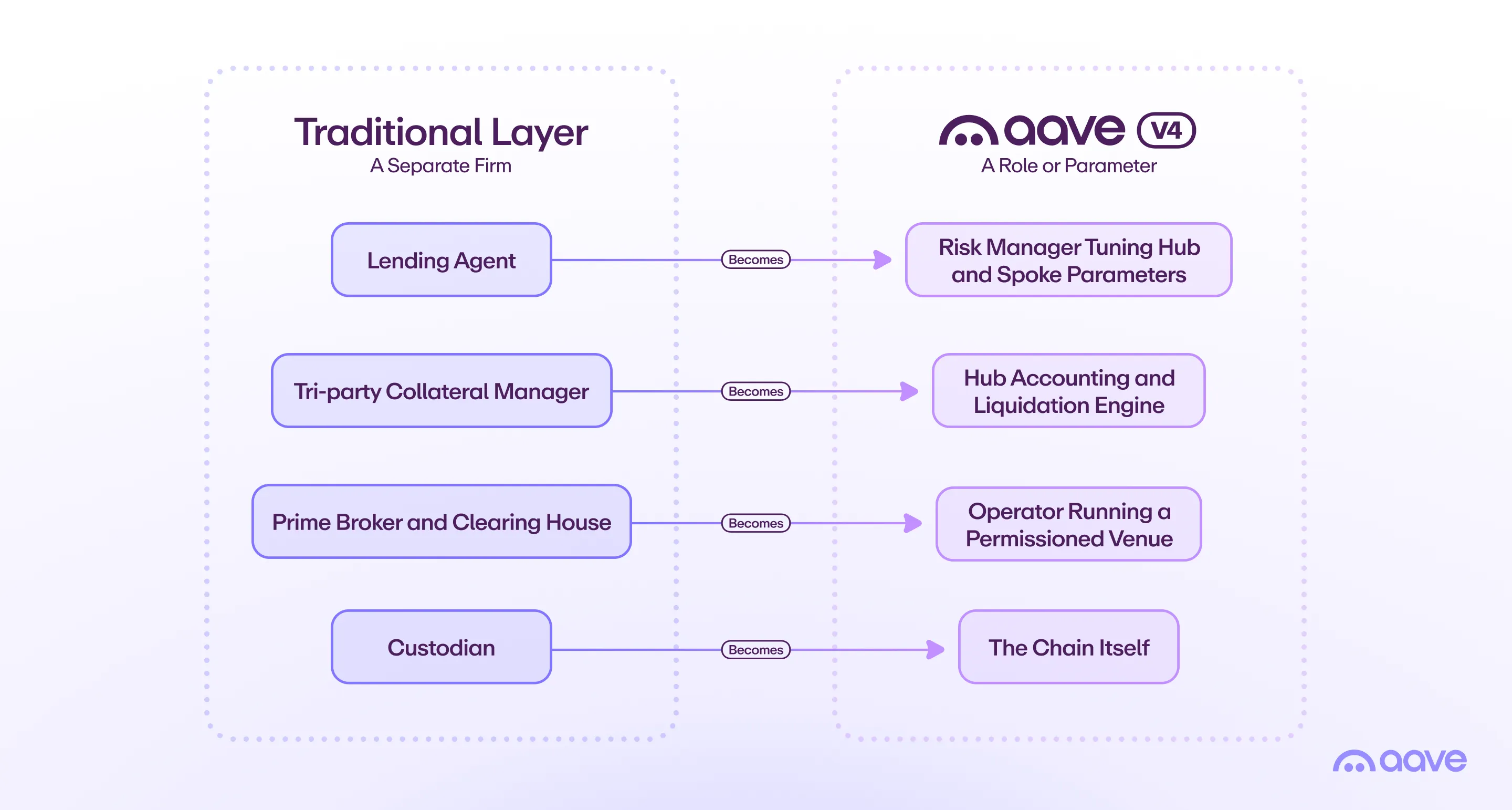

Roles, in either model

The firms that used to be separate layers become parameters and participants. The lending agent becomes a risk manager tuning hub and spoke parameters, the tri-party collateral manager becomes the hub's accounting and liquidation engine (the protocol itself), and the prime broker and clearing house become an operator running a permissioned venue. The custodian's ledger becomes the chain itself.

What changes structurally

The functions that used to live in separate firms move into protocol roles, so the work survives while the rent does not. Collateral that used to sit inside bilateral agreements goes to work, since the same asset can back exposure across every hub it qualifies for, no prefunded inventory parks at each counterparty, and no float bleeds yield. A permissioned spoke or a jurisdiction-scoped hub enforces KYC, jurisdiction, and eligible-asset rules at the edge while still drawing on shared liquidity, so a regulated institution gets a venue that fits its rules without fragmenting the order book the rest of the market relies on.

Settlement happens at a different speed entirely. Traditional securities markets still settle one day after the trade in the United States and two days after across much of Europe, and the industry's recent step to one-day settlement alone cost participants around $30 billion to implement. V4 settles atomically, around the clock, with no failures and near-zero marginal cost, and the reconciliation that takes days in traditional finance becomes a single state read onchain.

What it unlocks

For asset owners, borrowers, and cash lenders, the gains are concrete. The addressable market runs into the trillions, with repo averaging roughly $12.6 trillion in daily exposures in the U.S., margin at $1.3 trillion, and securities lending at $4.6 trillion on loan, all sitting on collateral headed toward $16 trillion tokenized by 2030.

Yield is kept rather than skimmed, since the 20 to 30 percent of securities-lending revenue that agents capture today routes back to the asset owner. Settlement no longer fails, because atomic, 24/7 delivery-versus-payment replaces the T+1 and T+2 cycles and the intraday failures that plague bilateral repo. Capital works harder, since pooled hub liquidity ends idle prefunded inventory and lets the same collateral move across venues. Risk becomes visible and contained, with positions, haircuts, and rehypothecation transparent in real time and category hubs keeping a shock where it starts. And access takes minutes, so an owner can borrow against tokenized holdings on demand at a transparent, market-set rate instead of negotiating a bilateral line over days.

The takeaway

Securities finance has been waiting for a settlement and collateral layer that can function without a stack of intermediaries. Securities-backed lending, repo, and securities lending are three faces of the same balance sheet, where you borrow cash against what you hold, finance it short-dated, or lend it out for yield, and together they move tens of trillions of dollars on plumbing that skims billions and settles in days.

V4 hosts all three on one architecture, whether that is a single deep hub or a mesh of category-and-risk hubs that spokes route across, with the liquidity, the stablecoin cash leg, and the institutional pipeline already live. The plumbing finally gets an upgrade, the value flows to the people who own the assets, and the market that runs on it is measured in trillions. This is the market Aave can capture.